Kevin Vaz, Kiran Mani, Sanjog Gupta to head 3 verticals of JioStar

Kevin Vaz, Kiran Mani, Sanjog Gupta to head 3 verticals of JioStar  Govt & industry to prime gaming space for global dominance: MIB Secy Jaju

Govt & industry to prime gaming space for global dominance: MIB Secy Jaju  Netflix ad-supported tier touches 70mn MAUs globally

Netflix ad-supported tier touches 70mn MAUs globally  Minister Murugan likens IFFI to Cannes fest; ‘Better Man’ opening film

Minister Murugan likens IFFI to Cannes fest; ‘Better Man’ opening film  Ali Fazal wraps up filming for ‘Metro In Dino’

Ali Fazal wraps up filming for ‘Metro In Dino’  ‘The Fable’ wins best film at the 38th Leeds International Film Festival

‘The Fable’ wins best film at the 38th Leeds International Film Festival  Sony SAB brings back ‘Tenali Rama’ at 8 pm slot

Sony SAB brings back ‘Tenali Rama’ at 8 pm slot  Zee Telugu to premiere ‘Aay’ on November 17

Zee Telugu to premiere ‘Aay’ on November 17  Release date of Pratik Gandhi, Divyenndu-starrer ‘Agni’ announced

Release date of Pratik Gandhi, Divyenndu-starrer ‘Agni’ announced

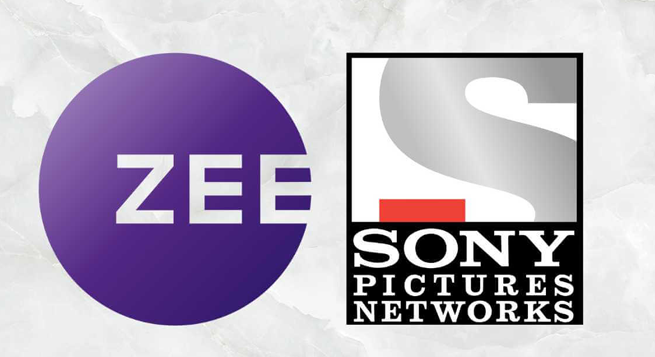

The National Company Law Tribunal (NCLT)’s approval for the Zee Entertainment-Sony merger without conditions offers further respite for Zee valuation, which has been muted for the past two years (the stock has not given any absolute returns).

The company will now move the Registrar of Companies to file for the merged entity once the final NCLT order is released. In the interim, we await the outcome of the SEBI and SAT cases against the Goenka family, the promoter, which may not have any adverse impact on the merger, as Punit Goenka has already stepped down from the Board.

In a worst case scenario, the Board and shareholders will appoint a new CEO in case SAT order is against Punit Goenka. Post the regulatory approvals, Zee will be delisted, and the merged company will be relisted as Sony-Zee wherein 100 shares of Zee will enable shareholders to get 85 shares of the merged entity (~2-3 months process).

We do not expect any change in the deal contours despite the long delay, as NCLT has approved the scheme. Further, Sony will get a majority shareholding of 50.8 percent in the merged entity whereas the Goenka family’s stake will move up to 3.99 percent, which includes the non-compete fee. We do not expect any impact from creditors filing a case against the NCLAT order.

Disruption Defining Merged Company Valuation: India’s OTT landscape has seen a disruption post JioCinema offering OTT content free of cost, which has led to other platforms reducing average revenue per user (ARPU) or offering content free; unit economics are already not in favour of OTT, and free content offering will further delay the path to profitability for OTT firms.

Further, Zee also has bought TV rights of the ICC tournaments from Star-Disney, which too will see lower revenue than our expectations — we have cut our sports revenue estimates by 15-20 percent, on the back of a volatile ad environment on TV in the near term.

Another big factor, which remains favourable for Zee-Sony, is the potential exit of Disney from the TV landscape. In case of a strategic partner or an exit by Disney-Star from India’s TV business, Zee-Sony may find it easier to displace the former to achieve the No. 1 position in the TV broadcasting space.

Moat Remains for Merged Firm: Zee-Sony commands an ad market share of 24 percent as on CY22, below the other large peer, Star-Disney, which is at 33 percent; formation of a large entity on the broadcasting side would lead to cost and revenue synergy, which would offset the negative impact of lower growth rates (India TV ad revenue CAGR has been flat over FY20-23).

Merged OTT Platform; Better ARPU: Both OTT platforms (SonyLIV, Zee5) coming together would help the merged company gain further market share in the digital segment too, as it has a variety of catalogue with little overlap on digital content, just as in TV.

The OTT business is all about scale and a merged OTT platform would lead to better ARPU/ad led revenue growth coupled with an improved distribution mechanism and revenue too.

It also can lead to efficiency on cost, which, in turn, could reduce losses. The merged company also will look to enhance its offerings in the sports (cricket) segment, which is the fastest-growing genre, both on TV and digital, helped by increased consumption patterns.

(The views expressed in the write-up are those of the author.)